🎉 Waltz reaches $50M💰 in funding to support LATAM growth 🎉 Read the full story here

Trying to get a loan for a rental property?

Your debt-service-coverage-ratio (DSCR) determines whether your rental income can comfortably cover your loan payments, and it’s one of the most important numbers lenders evaluate when approving financing.

But what if your DSCR comes in too low? Maybe your appraisal used conservative rent comps, or property expenses inflated your monthly debt. Whatever the cause, a weak DSCR can block loan approval or limit how much you can borrow.

This guide explains how to identify what’s pulling your ratio down and how to fix it. From adjusting rent and refinancing debt to exploring short-term rental income, you’ll learn practical ways to strengthen your DSCR to improve your chances to qualify.

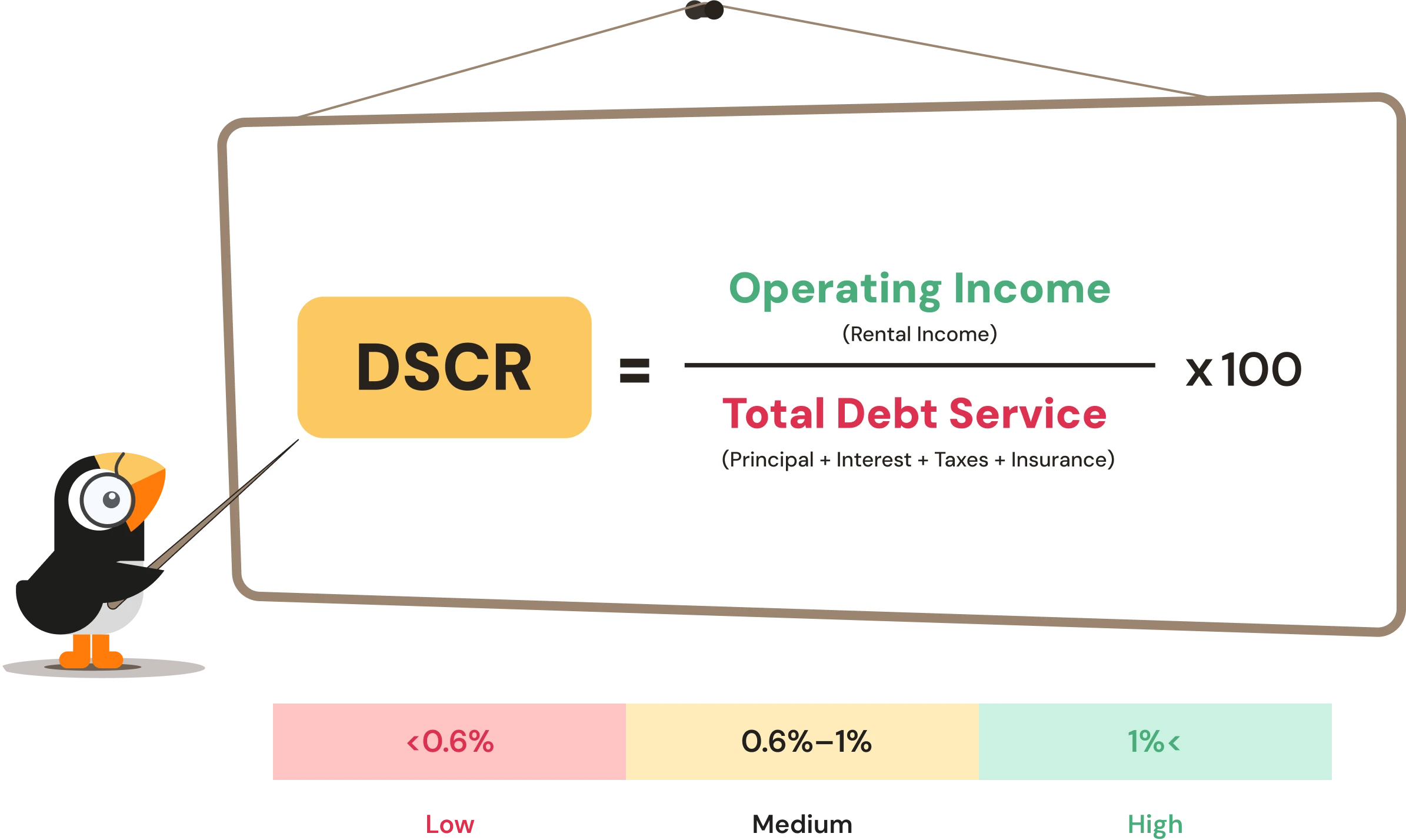

Debt-service-coverage-ratio (DSCR) is the key metric lenders use to evaluate whether your rental property generates enough income to cover its monthly loan obligations. In simple terms, it’s a snapshot of your property’s financial health.

Debt-service-coverage-ratio = Rent / Total monthly debt service

(where Total Monthly Debt Service = Principal + Interest + Taxes + Insurance + HOA, if applicable)

If your DSCR equals 1.0, it means your rental income just covers your monthly expenses. A 1.25 DSCR means your property generates 25% more rent than it owes, signaling stronger cash flow and lower lending risk.

Most lenders, including Waltz, look for a DSCR above 1.0 to approve a loan. The higher your ratio, the better your financing options, from lower rates to higher loan-to-value (LTV) thresholds.

Understanding this ratio is the first step toward improving it because once you know which side of the equation is underperforming (income or expenses), you can take strategic action to fix it.

Learn more: DSCR Loan Calculator

A low DSCR doesn’t always mean your property is unprofitable, but it does signal that lenders may see it as higher risk. Understanding why your DSCR came in below expectations helps you pinpoint what to adjust.

If your rent is below local market averages, your income side of the DSCR equation will lag. This is common when investors inherit long-term tenants or underprice units to attract occupancy. Comparing your rent against similar properties in your area is the first step toward identifying missed income potential.

In DSCR lending, lenders often rely on market rent, not your actual rent roll. If an appraiser selects overly conservative comparable properties (comps), your DSCR can drop. Reviewing appraisal comps or appealing to include stronger rentals in the report may improve your score on refinance.

Rising property taxes and insurance premiums can significantly increase monthly debt obligations, lowering your DSCR even when rental income remains stable. This is especially common in coastal or high-growth states where valuations and coverage costs rise faster than rents.

A 15-year loan or a higher interest rate increases your monthly debt service. Extending to a 30-year term or refinancing into a lower rate can immediately lift your DSCR without changing rent.

Once you know what’s pulling your DSCR down, you can take targeted steps to fix it. The key is to either raise your rental income or reduce your monthly debt service, and in some cases, both.

If your rent is underpriced compared to similar properties, adjusting rates is often the fastest path to improvement. For long-term tenants, consider incremental increases aligned with market standards or upgrades that justify higher rent.

Short-term rentals (STRs) can significantly boost gross income if local laws allow them. Platforms like Airbnb and Vrbo often command higher monthly rents, especially in tourism-heavy areas. Waltz supports DSCR loans for short-term rentals, giving investors flexibility that many lenders don’t.

Reducing your interest rate or extending your loan term immediately lowers monthly debt service. For example, shifting from a 15-year to a 30-year term can increase DSCR by lowering the denominator of the equation.

Look for recurring expenses that can be trimmed, such as management fees, maintenance contracts, or landscaping. Small savings add up and can meaningfully raise net income.

If you’re still in escrow or negotiating financing, increasing your down payment reduces your loan amount and, in turn, your monthly debt service. It’s one of the most straightforward ways to improve DSCR before closing.

Where zoning allows, converting a garage, basement, or detached structure into a second rentable unit can substantially increase income while keeping expenses relatively flat. This strategy is especially relevant if you already own the property and are refinancing, as it can boost cash flow and improve your DSCR. It is less applicable when purchasing a new property, since the conversion would not yet be generating rental income.

Even if your DSCR is below 1.0 today, there is often a path forward with the right adjustments. Improving your debt-service-coverage ratio not only makes your loan application stronger but also unlocks better terms, higher leverage, and greater portfolio potential. Whether it is adjusting rents, refinancing to boost cash flow, or exploring short-term rentals, small changes can have a big impact.

Waltz takes the guesswork out of the process. Our team works closely with investors to explore different scenarios, combining DSCR-based financing, refinance strategies, and cash flow modeling so you can see exactly how each adjustment affects your loan eligibility and potential returns.

Get started with Waltz

Fill out a quick form and we'll get back to you shortly.