🎉 Waltz reaches $50M💰 in funding to support LATAM growth 🎉 Read the full story here

Short-term rentals (STRs) such as Airbnb, VRBO, or fully furnished nightly rentals are an increasingly popular strategy for foreign nationals investing in U.S. real estate. In tourist destinations like Florida, these offer strong cash flow potential.

But while the appeal is clear, financing short-term rentals has been anything but simple for international buyers. Traditional lenders often exclude STRs from their underwriting, require U.S. credit or residency, or insist on in-person branch visits. That leaves many investors assuming the only way forward is an all-cash purchase.

Debt-service-coverage-ratio (DSCR) loans change that. By qualifying based on projected rental income, not personal credit or income, they open the door for foreign nationals to finance vacation rentals without the usual roadblocks.

Short-term rentals (STRs), fully furnished homes or condos rented on a nightly or weekly basis through platforms like Airbnb or VRBO, have become a go-to strategy for many international buyers.

For foreign nationals, STRs combine strong financial upside with lifestyle flexibility. Florida’s beaches, Arizona’s desert getaways, and the Smoky Mountains in Tennessee and North Carolina are just a few examples of STR-friendly markets attracting foreign investors. With rising demand from both leisure and business travelers, STRs provide a way to generate income while still having a place to stay when visiting the U.S.

Short-term rentals (STRs) can require more oversight than traditional long-term leases, but for many foreign investors, the rewards far outweigh the effort. Beyond higher income potential, they offer financial, lifestyle, and even tax-related advantages.

While the upside is attractive, short-term rentals come with added complexity. For foreign investors, these challenges can feel even steeper without the right support team in place.

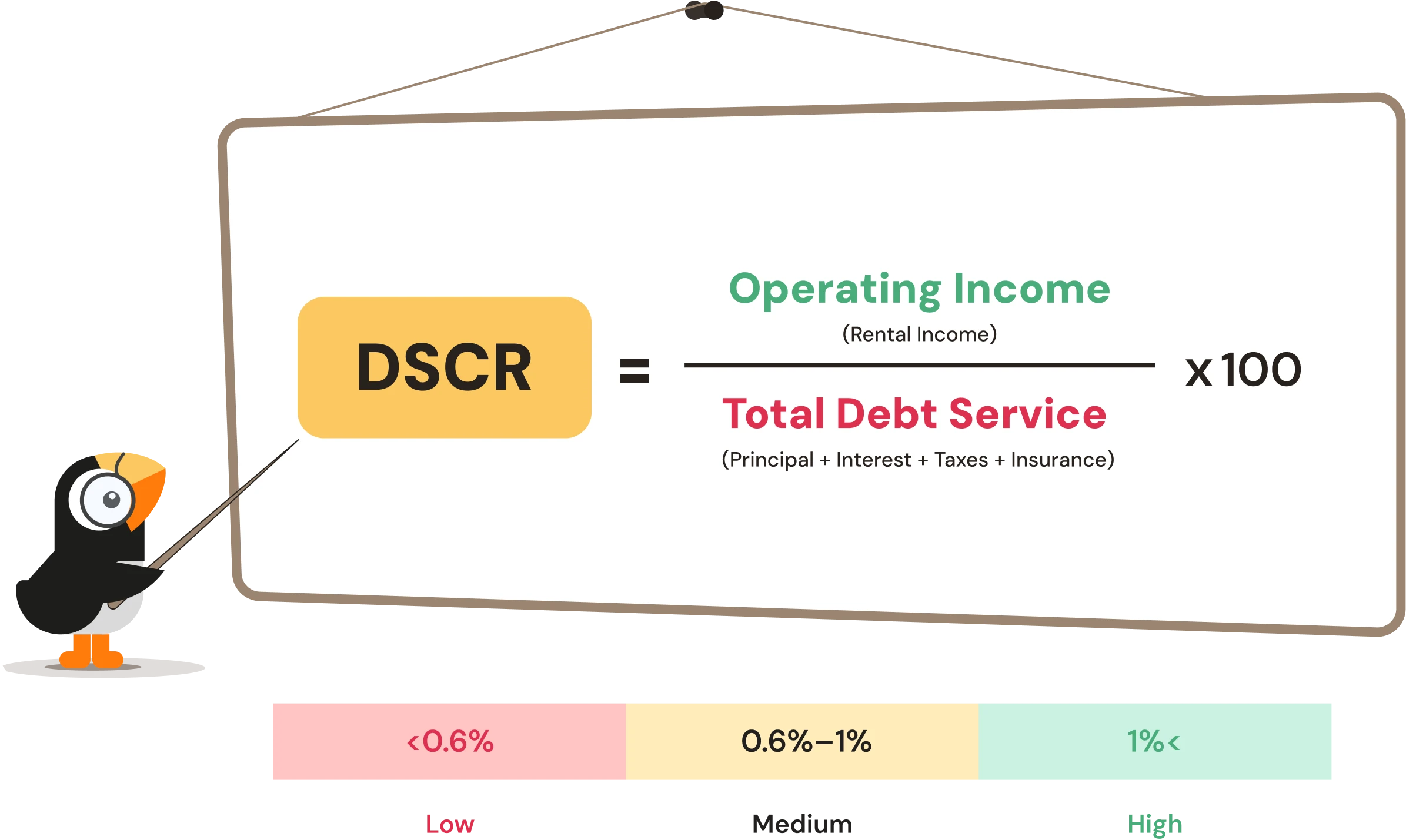

Traditional lenders rarely finance short-term rentals for foreign investors, but DSCR loans make it possible by focusing on the property’s income instead of the borrower’s personal profile. The DSCR calculation is straightforward:

DSCR = Operating Income ÷ Total Monthly Debt Service

(Where debt service includes principal, interest, taxes, insurance, and HOA fees if applicable.)

To qualify, the property must typically show a DSCR of greater than 1.0, meaning projected rent covers at least 100% of monthly expenses.

Unlike long-term rentals, where banks look at existing leases, STR underwriting relies on projected rental income. Appraisers and lenders use tools like AirDNA data and the income approach to estimate what the property can reasonably earn on platforms like Airbnb or VRBO.

For foreign investors, this approach is essential. It means you don’t need U.S. credit, tax returns, or income verification, only a property with strong rental projections and proper documentation.

If you’re considering financing a short-term rental in the U.S., here’s a simple roadmap to follow:

Short-term rentals combine lifestyle flexibility with strong income potential, which explains why they’ve become a top choice for foreign investors in U.S. real estate. The challenge has always been financing: traditional lenders either exclude STRs or impose requirements that most international buyers can’t meet.

DSCR loans change that, and Waltz makes them accessible. By qualifying based on projected rental income and bundling LLC formation, EIN setup, and more into one digital process, Waltz removes the friction that typically slows down foreign investors. Finance fast and close remotely so you can start hosting guests sooner.

Ready to finance your short-term rental in the U.S.? Get started with Waltz

Fill out a quick form and we'll get back to you shortly.