🎉 Waltz reaches $50M💰 in funding to support LATAM growth 🎉 Read the full story here

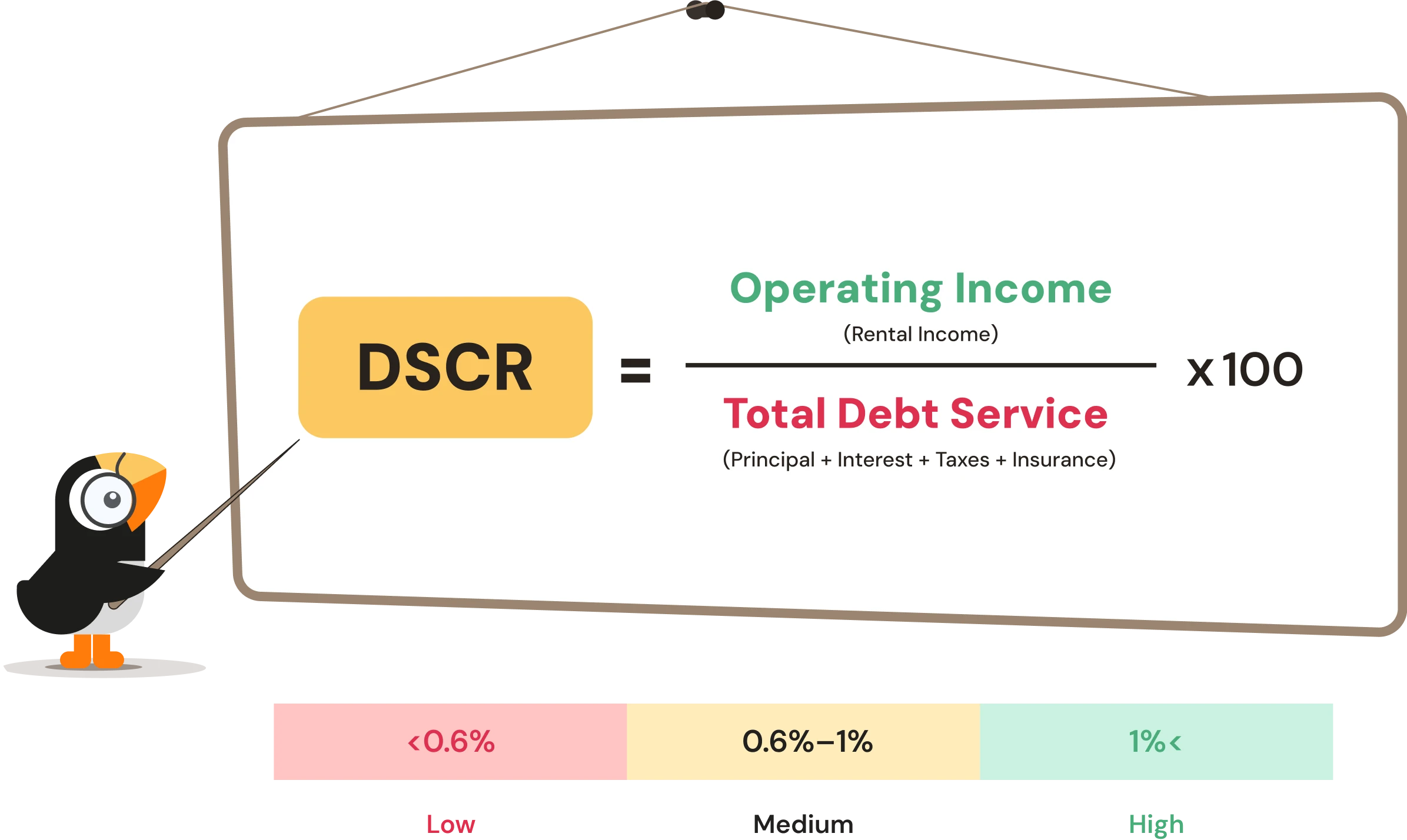

DSCR– the four letters every foreign real estate investor should know. Standing for debt-service-coverage-ratio, this figure tells lenders whether your rental income can cover the monthly mortgage payment. At Waltz, it’s the core factor we use to qualify you, not your personal income or U.S. credit history. To qualify for a DSCR loan, your rental property needs to have positive cash flow with a DSCR above 1.

So, how do you calculate it? It comes down to a simple formula—and once you know it, you can figure out your DSCR in seconds. Here’s how it works.

The DSCR formula is simple and Waltz keeps it even simpler than most lenders:

There’s no need to subtract property management fees or calculate operating expenses. At Waltz, we focus on how much the property brings in each month versus what it costs to own and finance it. As long as your monthly rental income is greater than your monthly mortgage payment, your deal is on solid ground.

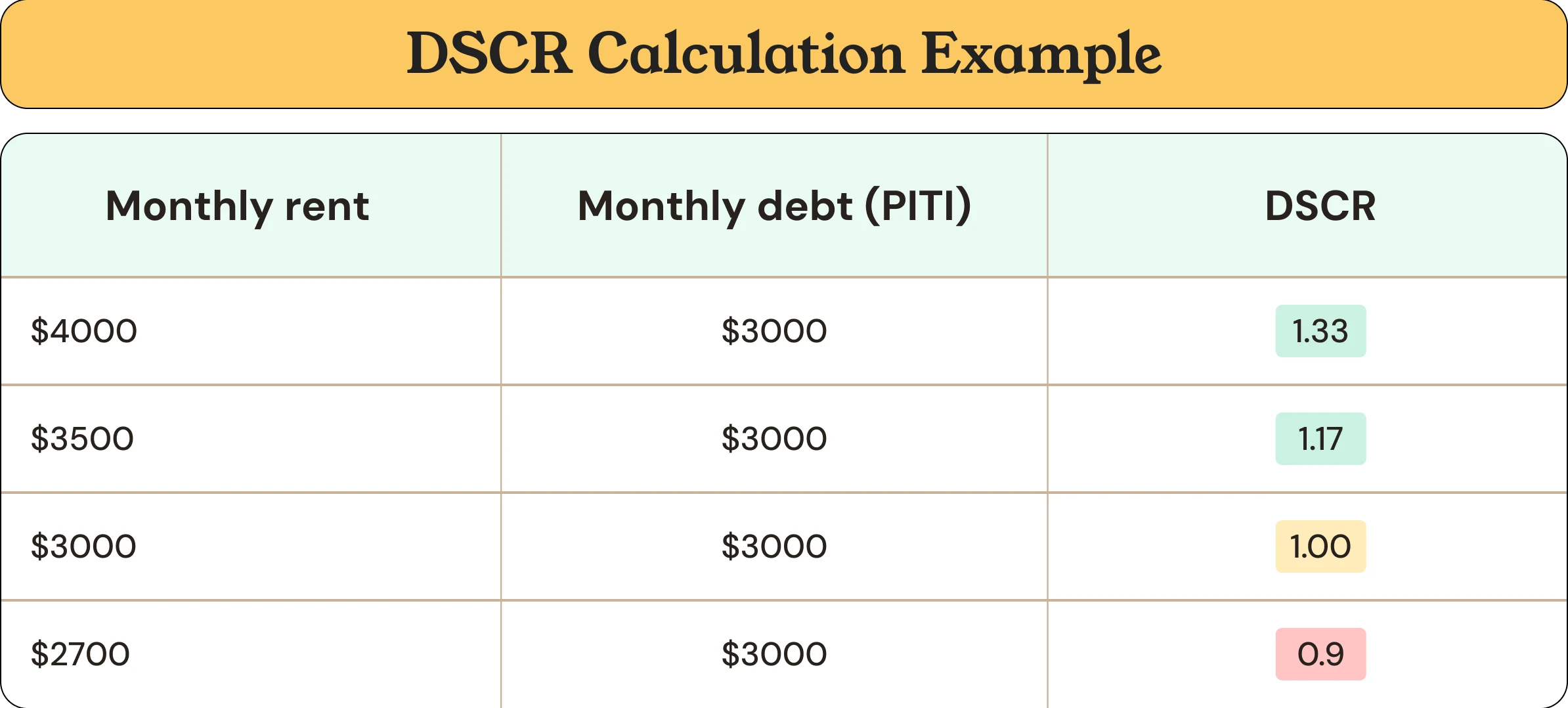

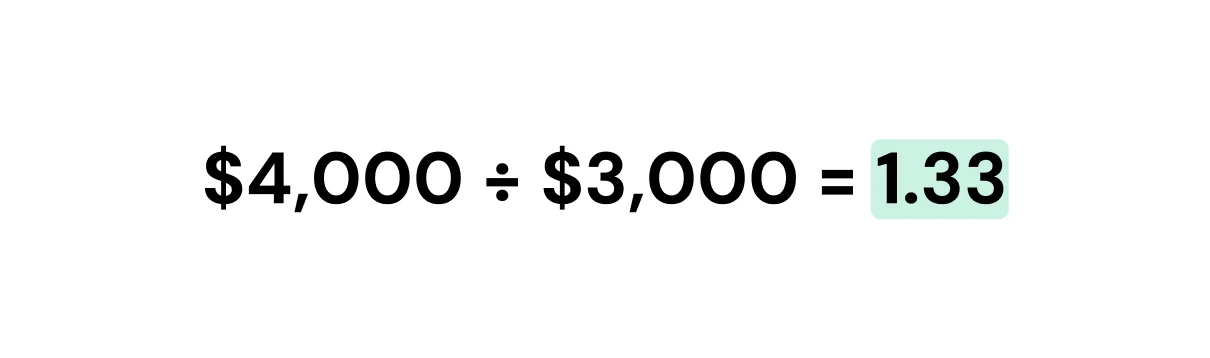

Let’s say you find a rental property in Miami that earns $4,000/month in rent. If your monthly mortgage payment (including taxes, insurance, and HOA fees) is $3,000, your DSCR would be:

Learn more: DSCR Loans for Foreign Nationals

When calculating your DSCR, there are only two numbers you need: your expected monthly rental income and your monthly mortgage (debt) payment. Here's how Waltz evaluates each one.

Waltz uses the property’s full monthly rent. If the property already has tenants, we use the lease to project cash flow. If it’s vacant, we estimate market rent.

Considering a short-term rental? We can also use projected income from rental platforms like Airbnb. It’s not net operating income or anything complicated. At Waltz, your DSCR is simply the amount of rent the property generates divided by the monthly cost of ownership.

Your monthly mortgage payment includes:

Waltz estimates these numbers early in the process, so you’ll know quickly whether a property is likely to qualify.

At Waltz, the minimum qualifying DSCR is 1. That means the property’s rental income must at least cover the full monthly mortgage payment, including principal, interest, taxes, insurance, and HOA if applicable.

A DSCR above 1 is ideal because it shows the property generates more income than it costs to operate. The higher your DSCR, the less risk the lender takes on, and the stronger your application looks. In some cases, a higher DSCR can even help you qualify with more favorable terms.

Sometimes the math protects you from taking a bad deal. DSCR isn’t just a lender’s tool, it can help you avoid buying a rental that’s likely to lose money.

Learn more: What You Need to Know Before Applying for a DSCR loan

If your DSCR is just below 1, or you want to strengthen your position, here are five ways to improve it before applying:

Learn more: Apply for a DSCR Loan as a Foreign National

With Waltz, calculating your DSCR isn’t guesswork, it’s built into the process from day one. As a foreign national, you don’t need U.S. credit, tax returns, or even a U.S. income history to qualify. All you need is a property that cash flows. Here’s what makes Waltz different:

Ready to qualify based on your property’s income, not your own? Waltz makes it possible. Whether you're investing in a long-term rental or short-term Airbnb, we’ll help you estimate your DSCR, set up your U.S. entity, and close — all without stepping foot in the country.

Fill out a quick form and we'll get back to you shortly.