Buying real estate in the U.S. doesn’t have to be complicated—even if you’re investing from abroad. Single-family houses are one of the most common and in-demand property types for international investors, especially when paired with the right financing.

This guide will walk you through the investment journey step-by-step—from financing options to closing remotely with Waltz.

Key takeaways

Single-family houses are the most common property type in the U.S. and offer flexible exit strategies from renting to resale.

DSCR loans help you qualify for financing based on the property’s projected rental income, not your personal income or U.S. credit.

You can finance up to 70% of the purchase price and close in about 30 days—from anywhere in the world.

Why single-family houses appeal to international investors

For many foreign nationals, single-family homes provide the most accessible entry point into U.S. real estate. They're widely available, appealing to family renters, and easier to manage than multifamily properties or larger buildings.

Here’s why they’re worth considering:

Strong and consistent rental demand: In cities, suburbs, and even smaller towns, single family rentals remain in high demand, especially from long-term tenants looking for more space and privacy such as families with children.

Less complexity: Unlike condos or townhouses that operate within the rules of a homeowners' association (HOA), single-family houses give investors more control over the property. The absence of HOA rules makes remote ownership much more straightforward for international investors, giving you greater flexibility and control from afar.

Flexible resale opportunities: Before purchasing a property, it’s essential to consider multiple exit strategies. When the time comes to sell, you want assurance that the property will attract buyers. Single-family homes have broad appeal, attracting both owner-occupants and landlords alike.

Whether you're buying in Florida, Texas, or the Midwest, single-family houses offer a strong entry point for building a U.S. portfolio.

What type of loan is best for buying a single-family rental?

Choosing the right financing depends on your residency, credit history, and long-term investment goals. Below are the most common loan types for buying a single-family rental, starting with the one best suited to foreign nationals:

DSCR (debt-service-coverage-ratio) loans: DSCR loans are investment property loans that focus on the rental property’s income—not your personal income or credit history. As long as the projected rent covers the mortgage payment (typically with a DSCR of 1or higher), you may qualify.

Conventional loans: These often require U.S. residency, a domestic credit score, tax returns, and W-2 income. If you're living and working in the U.S., this may be an option if you have a debt-to-income ratio that aligns with your lender’s needs. For international investors, though, it's usually a long and unrewarding process.

Portfolio loans: Offered by lenders who keep the loan in-house, these are more flexible than conventional loans but may come with higher rates. They’re used in situations where the borrower or property doesn’t meet standard criteria.

Cash-out refinance: Already own a U.S. property? A DSCR-based cash-out refinance helps you access your equity and reinvest it into your next deal.

Hard money loans: These short-term loans are designed for speed, not long-term holding. They may work if you’re flipping or rehabbing, but come with high fees and interest rates that aren’t suited for rental property investors.

For many international buyers, conventional mortgages aren’t an option. However, that doesn’t mean you need to pay all cash. Many foreign nationals find that DSCR loans offer a combination of flexibility, speed, and scale, without requiring a U.S. financial footprint.

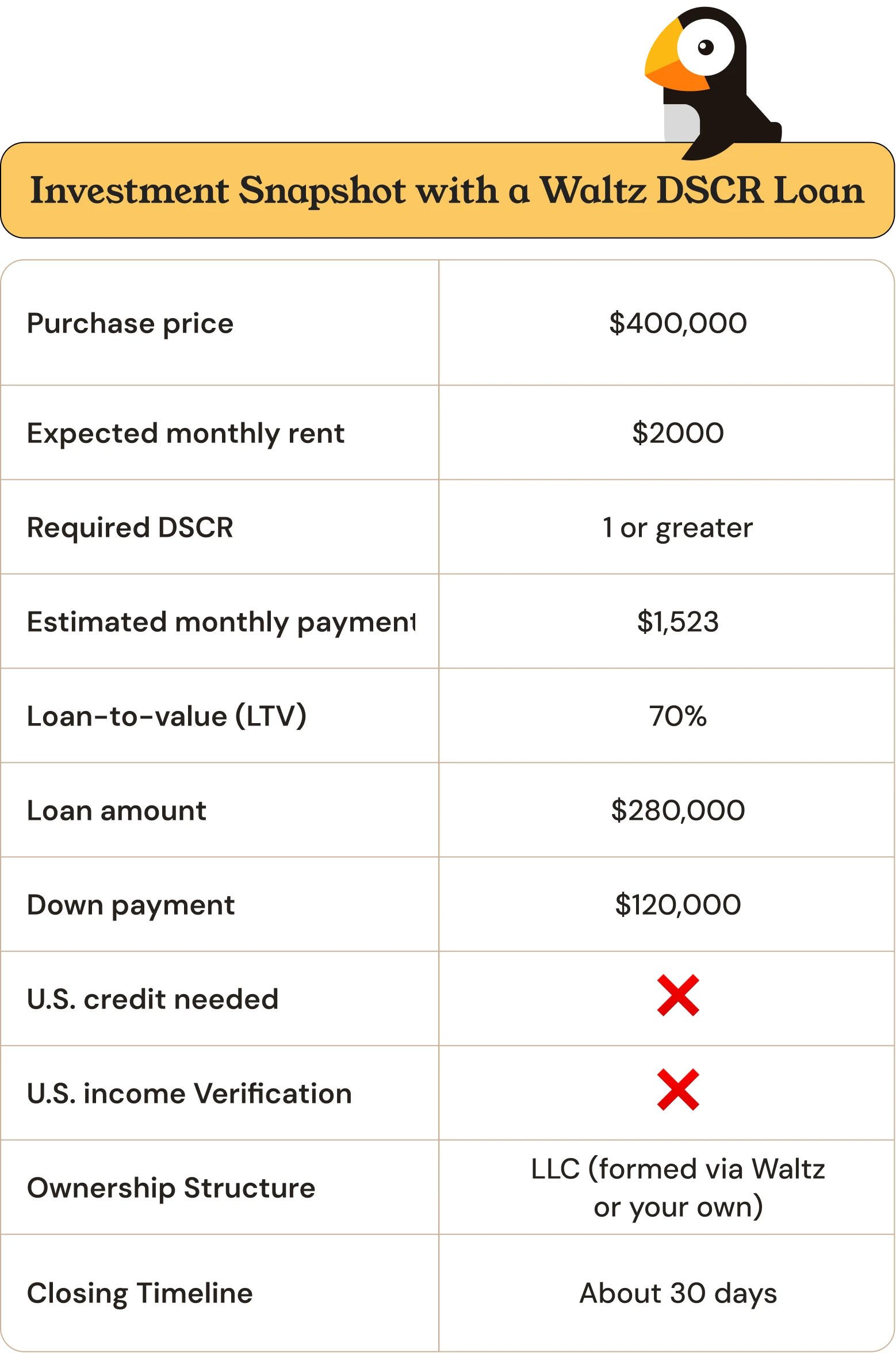

DSCR loan scenario: a single-family rental investment

Let’s walk through a real-world example of how a DSCR loan might work when financing a single-family property. Imagine you're purchasing a three-bedroom property in a strong rental market. The house is priced at $400,000, with projected rent of $2,000 per month. If your monthly mortgage payment is around $1,523, your DSCR would be 1.2, likely enough to qualify.

With this structure, you’re financing based on the rental income, not your personal finances. That opens the door to building a U.S. portfolio without needing to establish credit or income in the country.

The streamlined approach to single-family investing in the U.S.

Buying real estate in the U.S. as a foreign national can feel like you’re solving a puzzle with half the pieces missing. Most banks won’t lend to you without a U.S. credit score, verified income, and years of tax history. Even if you have the capital and the motivation, you’re often told “no” before you can even make an offer.

That’s where Waltz DSCR loans change the equation:

No U.S. income required: DSCR loans are based on the property’s rental income, not your personal earnings. That means you don’t need U.S. tax returns or domestic income to qualify. Waltz supports this further by accepting international documents like pay slips and bank statements from your home country.

No U.S. credit score needed: Most lenders won’t move forward without a U.S.-based credit history. Waltz takes a different approach, accepting credit reports from your home country and evaluating your overall financial strength with an international lens.

Lower down payments and flexible reserves: While most lenders require foreign nationals to put down 30–50% and hold substantial reserves, Waltz offers down payments starting at just 30% and can be flexible with reserve requirements–typically requesting six months worth. Your financial profile and the property’s projected income help shape what’s required.

If the property cash flows, we can help: DSCR loans are approved based on the property’s ability to cover its own expenses, typically requiring a DSCR of 1 or higher depending on the situation. If the rental income exceeds the costs of owning the property, you're in a strong position to qualify.

To finance a single-family rental using a DSCR loan, most lenders require the property to be owned by a U.S. business entity such as an LLC. That legal structure protects your assets and makes you eligible for financing, but setting it up on your own from abroad can be slow ,expensive, and complicated.

That’s why Waltz offers an add-on that allows you to get everything in one place with our Investor Kit:

Registered agent and digital mail services (1 year included)

U.S. bank account through Regent Bank2

Most foreign investors wait weeks, sometimes months, for these steps. With Waltz, most of this can happen in just minutes–all without setting foot in the United States.

A single-family rental can be your gateway into U.S. real estate if you have access to the right financing. Waltz makes it possible for people just like you. Apply now and take the next step toward building your U.S. real estate portfolio—wherever you are in the world.

Share this post on socials

Never miss an update

Stay informed and inspired: subscribe to our newsletter for exclusive updates, insights, and more!